In short:

- The invasion of Ukraine continues, as markets adjust to a heightened level of uncertainty

- China lockdowns dampen the energy demand outlook

- The bond market is beginning to price in a Fed policy error

As Russia’s invasion of Ukraine enters its sixth week, market participants are faced with several new realities that have both short- and long-term consequences.

First, regardless of how the invasion of Ukraine is resolved, economic sanctions against Russia are likely to remain for as long as Putin remains in power. This means that Russia will be a much-diminished economic power, as sanctions strip it of critical technologies. Second, prioritising the reduction of reliance on Russian energy will accelerate investment in renewable energy in Europe and elsewhere. Third, the sharp rise in critical grain and other commodity prices will challenge policy makers in emerging markets, where higher food prices will have a disproportionate impact. Finally, increased focus on the security of supplies will accelerate the existing trend towards greater diversification of supply chains.

These new realities are likely to dominate the long-term trends for commodity prices, global trade, and domestic industrial production. In the shorter term, however, other factors will also play a critical role. For example, oil, European natural gas and wheat prices have all come off their recent highs but remain very elevated by historical standards.

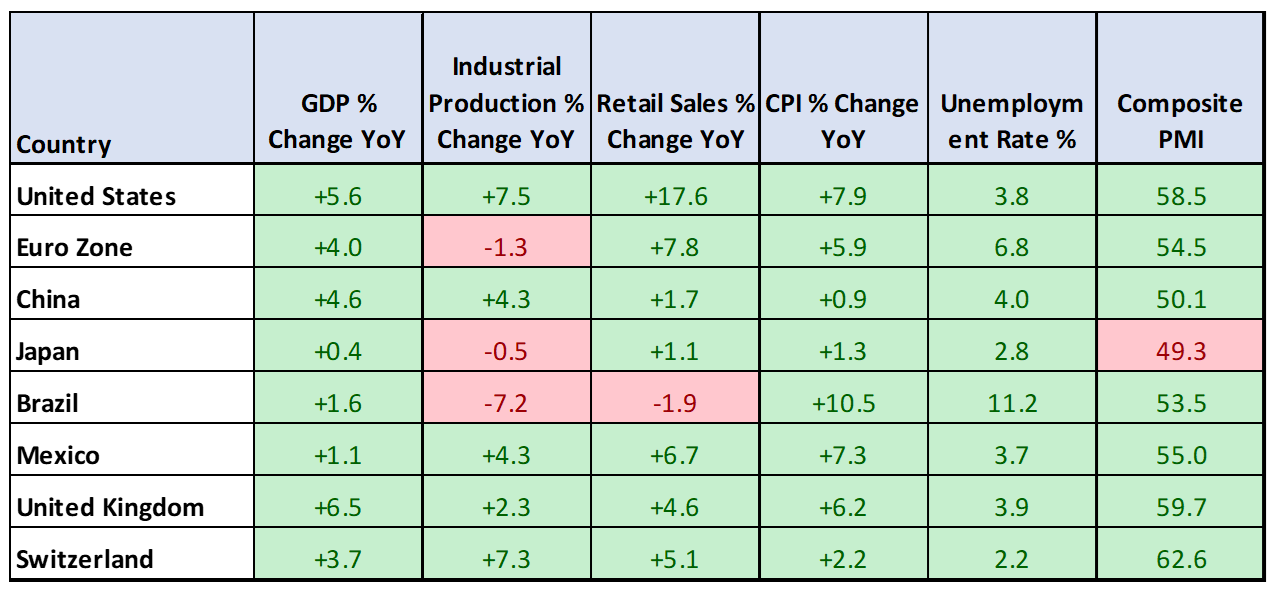

Source: Bloomberg

Part of the reason for the recent pull-back in energy prices is due to demand concerns from the world’s largest crude oil importer: China. The country is facing its worst Covid-19 outbreak since the pandemic began. China’s zero-Covid stance is one of the world’s strictest virus elimination policies. Whilst it helped the country rebound from the initial shock of the pandemic in early 2020, the longstanding effects of low community antibody levels are now being felt. Shanghai will be locked down in two stages over nine days, whilst authorities carry out testing. This follows provincial level lockdowns earlier this month.

Whilst long-term leading indicators have shown that GDP growth in the US and Europe has likely peaked and will continue to slow to below-trend in the quarters ahead, it remains robust for now. Inflation expectations in the US have begun to rise sharply, with the market derived expectations for inflation 2-years from now at around 5%. In Europe we are seeing a similar picture, with long-term inflation expectations signalling a strong fiscal response to the energy and defence crisis. This structurally higher inflation environment in Europe is a far cry from what ECB policy makers have come to expect over the last decade. A higher sovereign yield curve in Europe as a result of this new environment will place upward pressure on global bonds yields and could be part of the reason that we are seeing such a violent sell-off across the US Treasury curve. The sharp rise in yields in the front end of the curve has also driven a dramatic flattening, with the spread between the 2-year and 10-year bond approaching inversion territory.

The risk that the Fed will adopt a much more hawkish stance than originally anticipated, opting for 50bp hikes in all upcoming FOMC meetings, is starting to be fully digested by the bond market. Fed speakers seem to be ratcheting up forward guidance in this regard, by either publicly endorsing this decision, or not railing against it too strongly. The market is now pricing in around 240bp of total hikes by the end of 2022, an amount too large to accomplish with conventional 25bp hikes in the remaining meetings this year. With curves inverting, the treasury bond market is pricing in a potential policy error by the Fed. The Fed is forced to tighten into a slowing growth outlook, given the higher inflation expectations. With the natural rate of interest unknown, there is always the risk of the Fed tightening conditions too much – pushing the economy into recession.

Disclaimer:

Parkview Ltd (CRD 160171) and Parkview US LLC (160172) are registered investment advisors with the U.S. Securities and Exchange Commission (SEC). Parkview Advisors LLP is authorised and regulated by the Financial Conduct Authority (“FCA”). Registered Office is 8 Shepherd Market, Suite 5, London W1J 7JY. Parkview Ltd is a member of VQF (member number 13043). The VQF Financial Services Standards Association is organized under the terms of Art. 60 et seq. of the Swiss Civil Code (SCC) (established 1998), recorded in the Commercial Register of the Canton of Zug. VQF is the oldest and largest self-regulatory organization (SRO) pursuant to Art. 24 of the Anti-Money Laundering Act (AMLA) with the official recognition of the Federal Financial Market Supervisory Authority (FINMA). In addition, the VQF also has rules of professional conduct for asset managers which are officially recognized by FINMA and in this regard is active as an Industry Organization for independent Asset Managers (BOVV).

{kind=link}