Buy a cheap asset, watch it appreciate, and then sell it. What sounds like a simple and intriguing recipe for investment success is probably one of the most complicated to implement.

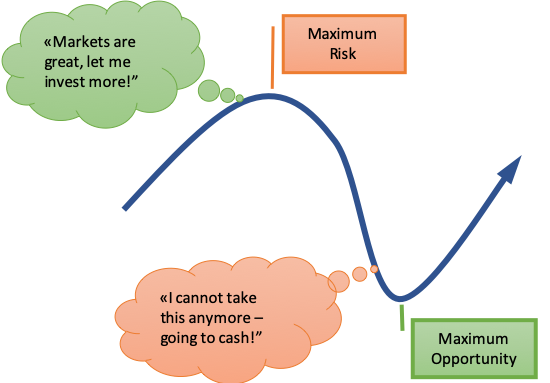

On one hand, we are neurologically coded to have greater risk appetite in bull and become more conservative in bear markets.[1] When our investment behavior is repeatedly rewarded with strong positive returns, dopamine drives us to take more risk as risk continues to build up. We feel good and “forget to sell high” as we pass the market peak or the point of maximum risk and with that the ideal moment to exit.

On one hand, we are neurologically coded to have greater risk appetite in bull and become more conservative in bear markets.[1] When our investment behavior is repeatedly rewarded with strong positive returns, dopamine drives us to take more risk as risk continues to build up. We feel good and “forget to sell high” as we pass the market peak or the point of maximum risk and with that the ideal moment to exit.

When markets crash on the other hand, we become increasingly risk averse. Market-induced stress is as much a psychological as it is a physical phenomenon and it is priming us to act.[2] An aversion to losses can be traced back to our ancestors, when running out of food proved to be fatal.[3] It was key to make quick decisions, cut losses and move on to new hunting grounds. As investors, when fear takes over, we exit risky markets. And as we approach the point of greatest opportunity, the point in the market cycle with the lowest downside risk and highest upside (again, something we can only identify in retrospect), we either sit on cash or more conservative fixed income investments, that tend not to participate in the subsequent market rally.

Whilst we have an urge to act, markets reward patience

Trying to time the market seems to be a legitimate tool to avoid periods of poor performance. However, consistent market-timing has proven to be extremely difficult and lack of success a significant source of underperformance. A 20 year buy-and-hold investor of the S&P 500 Index (1999 – 2018) would have earned an annual return of 5.6%. Missing out on only the 10 best out of 5,035 trading days would have yielded only 2% over the same period – an underperformance of 3.6%! Missing the 50 best days (less then 1% of total trading days) would have even resulted in a loss(!) of 5.9%.

Remember last year? In a volatile December of 2018, investors pulled close to USD 150 billion from actively managed funds, the biggest monthly outflow ever recorded by Morningstar, a fund data provider[4]. Subsequently, many of those investors were sitting at the sideline, flabbergasted, watching the markets rebound and culminating in the best January in 30 years.

With the benefit of hindsight, it would have been smarter to sit through the most recent market correction. How does last year compare to history? Since 1926, the US market lost 13 times 20% or more (on average 39%) and it took on average 22 months to recover losses. Not missing the first year of the recovery was always key with an average growth of 47%.

Whilst emotionally unsettling, the most effective remedy to a market meltdown is remaining invested throughout the drawdown, as every missed positive trading day will inevitably delay the full recovery.

Alternative: Strategic Investing with a “Risk Budget”

We are riding the longest bull market in the history of the S&P 500 for more than 10 years already and the next bear market may just be around the corner (on average every 6 years). If trying to time the market destroys value, how else can an investor prepare?

The key is to take an optimal amount of risk in the first place and that comes down to a personal choice. The objective is to design a portfolio one is willing to hold throughout a bear market and never feels compelled to liquidate. The maximum risk an investor is willing to take (e.g. “I never want to lose more than 20%”) defines the budget that can be spent. Subsequently, cash is deployed into different types of risky assets - the higher the risk, the higher the compensation we expect. From investment theory we know that with every uncorrelated asset we add to the mix we essentially reduce the portfolio volatility (risk), leaving more risk budget for inclusion of riskier assets with higher upsides. When selecting building blocks at Parkview, we tend to have a preference for conservative positioning, often reflected in superior “upside/downside capture”, rations that reveal, how active managers participated in up- (the more the better) and down-markets (the less the better). Another useful tool to protect the portfolio from the downside is insurance in form of “hedging”. When done partially, it can typically be implemented at zero cost, however it comes at the expense of only partial downside-protection and/or not fully participating in the upside.

Finding an optimal mix of risky assets is unfortunately not a one-time exercise. As risk/reward and correlations change, the asset allocation needs to be adjusted. Moreover, personal circumstances as well as preferences change and hence the original risk budget must be frequently revisited.

The primal fear that kept our ancestors alive, is keeping us from being successful investors. Being mindful of our coding and behavioral biases is a first and instrumental step to making sound investment decisions.

[1] Richard L. Peterson, The neuroscience of investing: fMRI of the reward system, Brain Research Bulletin, 2005

[2] John Coates, The Hour Between Dog and Wolf: The Risk-taking, Gut Feelings and the Biology of Boom and Bust, 2012

[3] McDermont, Fowler, Smirnov, On the Evolutionary Origin of Prospect Theory Preferences, The Journal of Politics, April 2008

[4] It is fair to point out, that passive funds had net inflows of almost USD 60 billion that month. However, that was significantly less than on an average month previously.

{kind=link}